Updated: March 29, 2023

Updated: March 29, 2023  1054

1054  11 min

11 min

45,000,000 Reasons There Is No Housing Bubble In 2023

A bubble is a term used to figuratively describe an inflating event with the perception it will burst. As an Indiana Realtor® I am here to burst your bubble: There is no housing bubble in 2023, and there won’t be one anytime soon. Just because prices are rising doesn’t mean there is a bubble.

The cottage industry of amateur economists has taken off in the wake of rapidly rising home prices starting in 2020. This surge of home prices has content creators and click-baiters flocking to YouTube, Tik-Tok, and every other low-cost platform espousing their beliefs home prices are in a bubble destined to burst and set home values back 20%, 30% or 50%.

They are wrong. There are 45,000,000 reasons why the U.S. housing market is not going to crash.

The Pinch Causing The Booming Housing Market Of 2023

I call the recent and rapid increase in U.S. home price prices the pinch. There are five distinct circumstances causing the pinch in the U.S. housing market.

1. COVID-19 Interrupted Major Life Events

Yeah, I am tired of blaming it all on COVID, too. But, this is legitimate. The U.S. housing market is driven by major life events. These include births & deaths, children growing up or moving out, new relationships, engagements, marriages, & divorces, and graduations, job placement, promotion, demotion, & relocation. A lot of this was delayed in 2020. But, now all the big events in life are starting up again. This is triggering demand in the housing market.

2. Long Term Low Interest Rates

Low rates means the cost of servicing the debt is less. Therefore, the seller can charge more for the underlying asset the buyer will borrow against. Pretty simple, right? Low rates push prices up.

3. Buyers Have Cash. Lots Of It.

Homebuyers, including plenty of first-time homebuyers, have the downpayment money. The number one issue with buying a first home is and always has been coming up with the down payment. But, this latest generation of homebuyers is less indebted compared to their parents. Time and again I have been really surprised at the number of 22 to 28 year olds wanting to buy a home who have the down payment and closings cost money.

But, now add in that shitshow which was 2020.

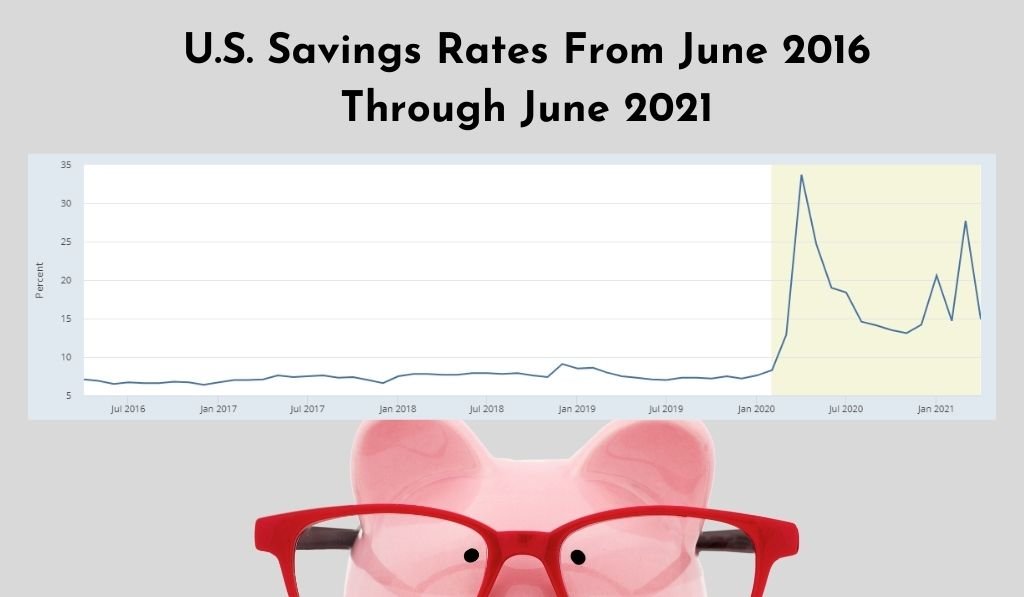

Do you know what the traditional savings rate is for Americans? And, do you know what it was in 2022 and the start of 2023? Plenty of wannabe homebuyers received stimulus checks, too. And more and more the bona fide economists are saying much of the money went right into people’s savings accounts.

U.S. savings rates in 2021 smashed the typical 4% to 8% monthly rate.

Lastly, current home owners have seen their home values only increase over the last ten years. This means their equity position has improved from both paying down the loan plus asset appreciation. This is giving current homeowners more cash to use for their trade-up home purchase for either the down payment or to lower the borrowed amount.

4. Not Enough Homes Were Built Between 2010 and 2020

Home builders simply have not built enough homes over the last ten years. The majority of the market still wants to own a single family home in a neighborhood with low crime rates and good schools. And there just are not enough of these homes to meet demand.

5. Demand Is Exceptionally High

There is crushing demand for new homes coming from many different population groups. 20 years ago we talked so much about prepping for the Baby Boomers and how they will dominate the economy. In all that discussion, I think we forgot about the tens of millions of Gen X, Millennials, and Gen Z. Have you seen these population numbers?

The Boomers want to downsize but want a nice, new home. Gen X is sitting pretty still right now. Plenty of the 72 million Millennials want to buy homes. The youngest Millennial is 25 years old by the way. Yeah, she’s ready to buy a house.

The 45,000,000 Million Reasons No One Is Talking About

The most important class to evaluate when predicting the near-in-time, future health of the U.S. housing market are people aged 25 to 34 years old. There are 45,578,475 people in that class.

There are more 25 to 34 year-olds alive today than there were 10 years ago. Today, this class makes up nearly 14% of the entire U.S. population. They are employed, have low debt-to-income ratios, and many stayed with their parents longer than their parents stayed with their grandparents. They’ve got the cash to close and they’ve got the credit and income to qualify for a mortgage. And they are here to buy your house.

Why 25 To 34 Year-Olds Are The Most Important Demographic To The U.S. Housing Market

People aged 25 to 34 place the most demand on the U.S. housing market and stimulate the most activity. First, Most people buy their first home between the ages of 25 to 34. So, currently the U.S. has this massive group of people buying from the market, but they are not giving anything back. To say this differently, there is no replacement. Because it is their first time on the merry-go-round, they are here to buy but have nothing to sell. This single taking from the market is a massive demand on the market.

Additionally, as people get into the early and mid-thirties there is an acceleration of people selling their first home and buying the second home they will own in their life. Whereas those in their 40s and 50s are more likely to stay put in what they already own. This is the squeeze.

As a real estate agent I have noticed this squeeze over the last four years. Each year, we are selling more homes than the previous year, but prices are still going up, homes are still selling fast, and there is always another buyer. Always. The market is just tighter and tighter each year.

And for all those “the sky is falling” naysayers. It won’t get better anytime soon. This is for two reasons.

First, despite a recent slowing population growth rate the U.S. added about 19,000,000 people in the last 10 years. People are living longer, immigration outpaces emigration, and procreation is always happening because plenty of people want to have kids.

Secondly, there will be a high number of people in the 25-34 year old age group for the next 15 years. Why you ask? Using that same 2019 U.S. Census Bureau data:

- 20 to 24 year-olds: 21.5 million

- 15 to 19 year-olds: 21.4 million

- 10 to 14 year-olds: 21.4 million

Younger than that we see about an 8% reduction in population starting at the age 5 to 9 age group. Those people who are currently 5 to 9 years old will just begin being buyers in 15 to 20 years.

The long, slow, recovery of the housing market and more specifically, the U.S. residential construction industry has set us back. The faucet left running of new home construction which ran from the 1960s until the mid-2000s slowed to a trickle.

Lack Of New Home Construction Supports High Home Prices

Simply, since the great recession of the mid and late 2000s we have not build enough homes for the U.S. population. Though home starts have been on the upswing for the last 10 years we did not build enough homes.

The decade started with home builders building between 400,000 and 600,000 new single family homes each year. Slowly, the trend went upward. From 2013 to 2017 600,000 to 800,000 new single family homes were built each year. Data confirms in the late 2010s the U.S. was building about 800,000 to 925,000 single family homes annually. At the end of the 2010s, we had built just 6.8 million new single family homes from 2010 to the end of 2019. The U.S. Census Bureau says we added 19,000,000 people in the U.S. during that same time.

2020 was a mess. I don’t think anyone knows for sure how many homes were built that year. Then, 2020 was chaos. Lots of new permits were issued, but there was also a lot of construction starts and stops. Overall, though, volume appears to be high. Consensus on March 2022 housing starts came in at an annual rate of 1.61 million and April 2022 1.71 million homes. Remember, housing starts are measured in seasonal adjusted annual rates (SAAR).

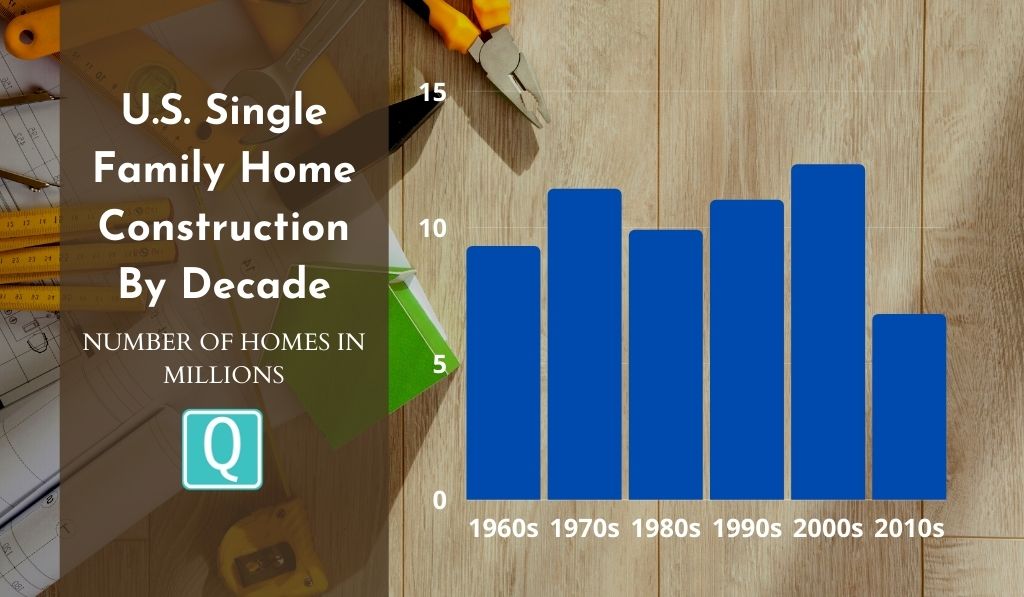

Overall, we are seeing a huge increase in new construction homes. However, there is years worth of catching up to do. In comparison, check out the number of new homes built during these other decades.

- 1960s: 9.3 million single family home builds

- 1970s: 11.4 million single family home builds

- 1980s: 9.9 million single family home builds

- 1990s: 11.0 million single family home builds

- 2000s: 12.3 million single family home builds

- 2010s: 6.8 million single family home builds

U.S Housing Market Prediction

The housing market has demand for single family homes will remain strong for years. New home construction will accelerate over the next ten years. Annual single family home construction will ebb and flow between 800,000 and 1,500,000 homes for the next five to ten years. Unforeseen major economic recessions could negatively affect this outcome, though.

Home prices will remain high, but most areas will not see a repeat of 10% to 20% annual appreciation in the coming years. Wages just are not rising fast enough to accommodate this. However, single family homes located in areas with low crime rates, good schools, and close proximity to jobs will continue to increase in value at slightly above average annual appreciation rates. These rates will likely be between 4% and 10%.

Should You Wait To Buy A House Until Next Year?

Nope. There is every indication homes will continue to increase in value in the short term future. Demand is high, inventory is low, and interest rates are low. There is no rationale which illustrates homes will be cheaper in the near future. All signs point to homes becoming more expensive in the near future.

Conclusion

The pontifications of a housing bubble and a pending real estate market crash are simply wrong. Housing is like food, water, and air. Shelter is a basic need needed by all people for the entirety of their lives.

It is certain the economy will ebb and flow from robust exuberance to cooler, calmer periods of slower activity. But a housing market crash is incredibly unlikely to occur. But, every yahoo with a camera, tripod, and microphone wants to talk about the pending U.S. housing market crash. Scroll through your favorite social media site and you’ll find these folks. Keep scrolling. They’re wrong.

Simply pointing to the housing crash of 2007 – 2010 and saying because prices are high today must mean the same will occur again today is an opinion which does not align with the facts. Tens of millions of people who today are between the ages of 15 and 34 will drive the housing market for the next 20 years.

About Quadwalls.com

Quadwalls.com is a real estate website designed to help homebuyers and sellers save money and make better decisions when buying or selling real estate. Additionally, the Quadwalls Connected Agents are a team of Northwest Indiana Realtors® here to help you buy or sell your home. We offer some of the lowest real estate commission fees in the region.