Updated: March 29, 2023

Updated: March 29, 2023  755

755  11 min

11 min

How Much Do I Need To Buy A House?

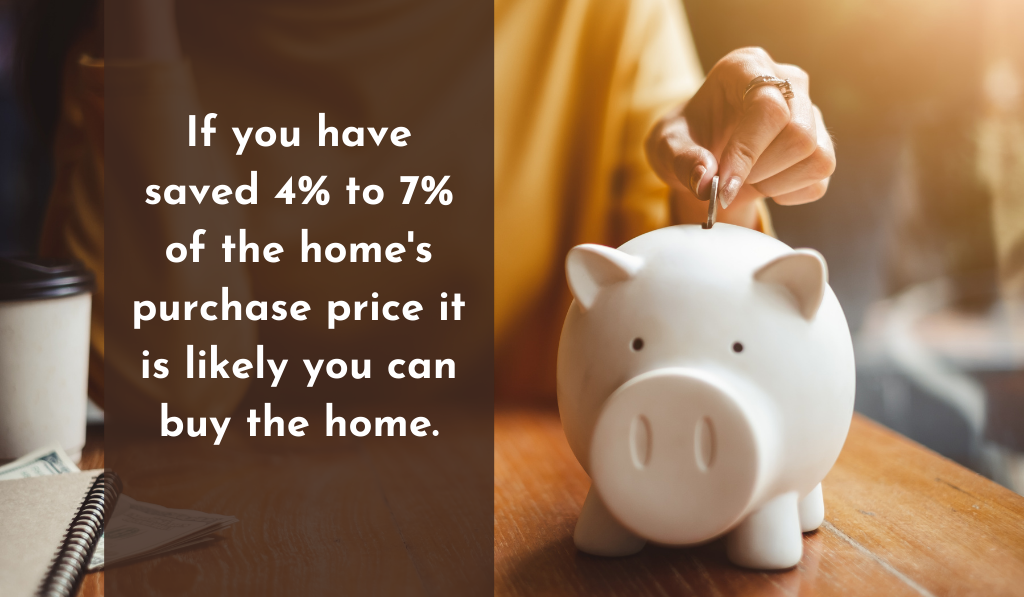

One of the first things I discuss with a new prospective homebuyer is their expectation about how much money you need to buy a house. I want to hear that the buyer has 4% to 8% of the home’s purchase price on hand. However, if the buyer is planning to use the VA or USDA 0% down payment programs, having 2% to 3% of the home’s purchase price is how much to save for a house purchase.

These are the numbers which get me to start my car and start showing some homes to the buyer.

So, if you are wondering how much money you need to buy a house the answer is 4% to 7% of the purchase price unless you are using a 0% down payment home loan product. In those cases, 2% to 3% of the purchase price provides enough room to get out there, find a home, and get it bought.

How do I get this answer? I did it through years of experience as a real estate agent helping hundreds of homebuyers, including many first-time homebuyers, find and buy homes. In this post I will describe how these different options affect how much money you need to buy a home.

Reading on will help you better understand your options and how to lower your cash to close requirements which is how much you need to buy a home.

How Much Money Should I Save Before Buying a House?

To provide some real examples of how much you should have saved before buying a house, I will use a home purchase price of $225,000. $225,000 is close to the median purchase price for first-time homebuyers in the U.S.

In this scenario a homebuyer using an FHA loan could buy the home with as little as $8,675 out of pocket if the buyer gets the seller to cover the closing costs. Buyers could close that same $225,000 home purchase with as little as $7,550 if using a 3% down conventional mortgage.

Alternatively, assuming you are looking at a home costing $150,000 a buyer could make this home purchase with just $6,050 using an FHA loan or $5,300 using a 3% down payment conventional loan. Notice how the significantly lower purchase price, 30% less than the first example, really did not reduce the cash to close and how much you need to buy a house by all that much.

Prospective homebuyers should save at least 4% of the home’s purchase price or more before starting to look at homes. As you increase your savings to 6%, 8% or even 10% of the purchase price of the homes you are considering I will tell you this: You don’t have anything to worry about. This is more than enough to get a home bought, so let’s go find you one to buy!

Expenses Affecting How Much You Need to Buy a House

There are three types of expenses which affect how much money you need to buy a house. These include transactional costs, down payment requirements, and closing costs. Below I will briefly explain each of these.

Transaction Based Out of Pocket Expenses When Buying a House

There are two common out of pocket expenses when buying a home with a mortgage which affect how much do i need to buy a house. These expenses are an inspection and an appraisal. A fair budgetary guideline for these items would be $800 to $1,350 for these items.

Homebuyers are not required to have a home inspection. However, many homebuyers do decide to have a home inspection. The cost for a home inspection varies depending on the home’s size and inspections you have completed. I advise home buyers to reserve $400 to $700 for home inspections.

Next, your lender will order an appraisal which will be charged to you regardless of if the home purchase closes. An appraisal by an appraiser selected by your lender is required for your loan to be approved. Appraisals vary depending on the loan type. However, I would budget $400 to $650 for your appraisal.

Your Mortgage Type Affects the Down Payment When Buying a House

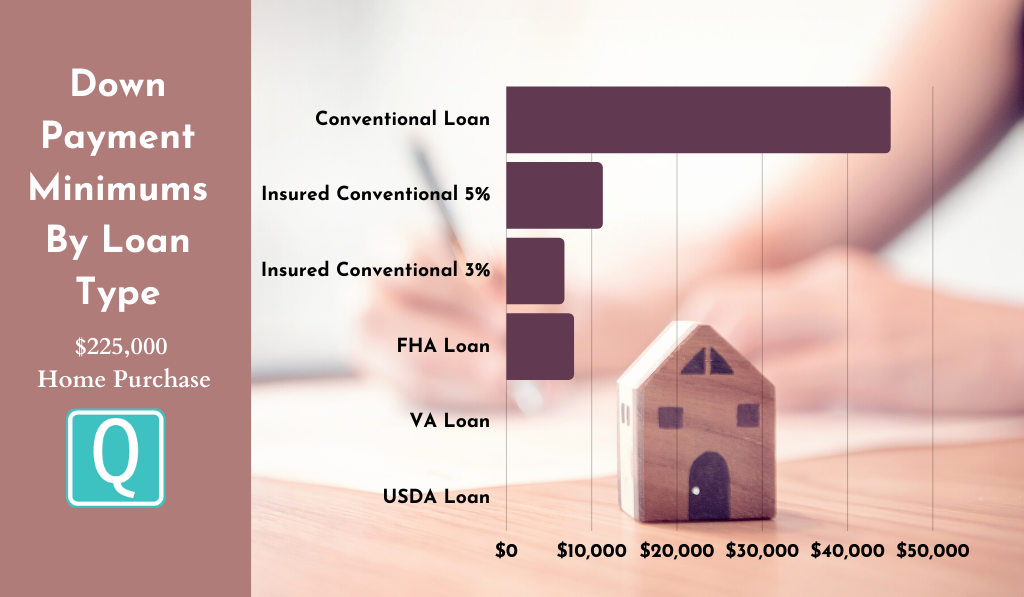

Conventional, insured conventional and the alphabet soup of FHA, USDA, and VA. Each of these are mortgage loan types. Moreover, each of these has a different minimum down payment requirement, and those affect requirements add to how much do i need to buy a house. Let’s briefly look at the minimum down payment percentages for five common home loan types.

- Conventional Loan: 20%

- Insured Conventional Loan: Typically 5%, but sometimes only 3%

- FHA: 3.5%

- VA: 0%

- USDA: 0%

Now that you know the different minimum down payment rates for the common home loan types you can see how much you need for the down payment on a house. I will work through an example with you.

Say you wanted to buy a $225,000, which is pretty close to the median purchase price for first-time homebuyers in the U.S. Below are the down payment requirements and the math for each common mortgage loan type.

- Conventional Loan 20% down payment: $225,000 x 0.20 = $45,000

- Insured Conventional 5% down payment: $225,000 x 0.05 = $11,250

- Insured Conventional 3% down payment: $225,000 x 0.03 = $6,750

- FHA Loan 3.5% down payment: $225,000 x 0.035 = $7,875

- VA Loan 0% down payment: $225,000 x 0.00 = $0

- USDA Loan 0% down payment: $225,000 X 0.00 = $0

Buyer Closing Costs When Buying a House

Closing costs are the last piece of what affects how much money you need to buy a house. Before I get to the explanation I want to give you a warning. Ignore advice from other writers and posts which encourage you as a “rule of thumb” to reserve a specific percentage of the purchase price as closing costs.

The problem with that advice is it is both a lazy and arbitrary way to total closing costs. Also, it is wrong. Many of the charges that make up closing costs are flat rate changes. Therefore, those costs are the same whether the home costs $100,000 or $400,000. So, a percentage based “rule of thumb” is really bad advice when trying to understand how much money you need to buy a house.

Closing costs are a total of the costs for loan origination, title company and governmental charges, as well as any administrative fee charged by your agent. Additionally, most homebuyers will pay the cost of the first year’s homeowner’s insurance premium plus impounds to begin funding your escrow account. Each of these increases your total cash to close and should be considered when determining how much to save for a house.

Closing costs for most homes will likely be between $3,900 to $5,400. The only effect of a substantially more expensive home is that the insurance and property taxes may be a bit higher. This will cause first year’s homeowner’s insurance and impound collections to begin funding the escrow account to be higher.

Closing Costs: Loan Production Charges

These are loan origination and processing fees. Frequently line items here include loan origination and production charges, other itemized fees from verifying the information you provided the lender, pre-paid interest on the loan, and impounds to begin funding the escrow account. Anticipate this portion of closing costs to total between $1,800 and $2,600.

Closing Costs: First Year Of Homeowner’s Insurance

It is common that a buyer pays for his or her first year of homeowner’s insurance at the closing table. Home insurance prices vary significantly. It is not so much the price of the home but more so the buyer’s insurance claims history, claims history on the property, and the age and location of the home. Looking at the median U.S. home in an average disaster prone area in the U.S. I would estimate $1,200 for this.

Closing Costs: Title Company Charges

Oftentimes there are a lot of line items for title company charges. However, most of those for a buyer are all pretty small. Title company charges can include a settlement fee, wire fees, transfer fees, and document fees, later-date title analysis fee, among others title analysis charges. Title charges will likely be between $600 and $900.

Closing Costs: Government Charges

The state and local governments often charge recording fees. These can include recording of the deed, the mortgage, and the sales disclosure. Homebuyers should budget between $100 and $300 for these charges.

Closing Costs: Miscellaneous Charges

The miscellaneous section really is a catch-all for any other charges unique to the specific transaction. The most commonly this will be an administrative fee charged by your real estate agent or the agent’s brokerage. $200 to $400 is a good budgetary number for miscellaneous charges.

Closing Costs: Conclusion

Assuming a median purchase price of $225,000 and the described charges, insurance, and taxes all within the range of what is standard and ordinary expect closing costs to be between $3,900 and $5,400.

Remember, just because a home has a substantially higher or lower purchase price does not mean closing costs will increase or decrease similarly. To say this differently, a home that costs twice as much as my example is very unlikely to have double the closing costs. It doesn’t work that way. This is why using a percentage of the home’s purchase price as a guidepost for the closing cost total is bad advice.

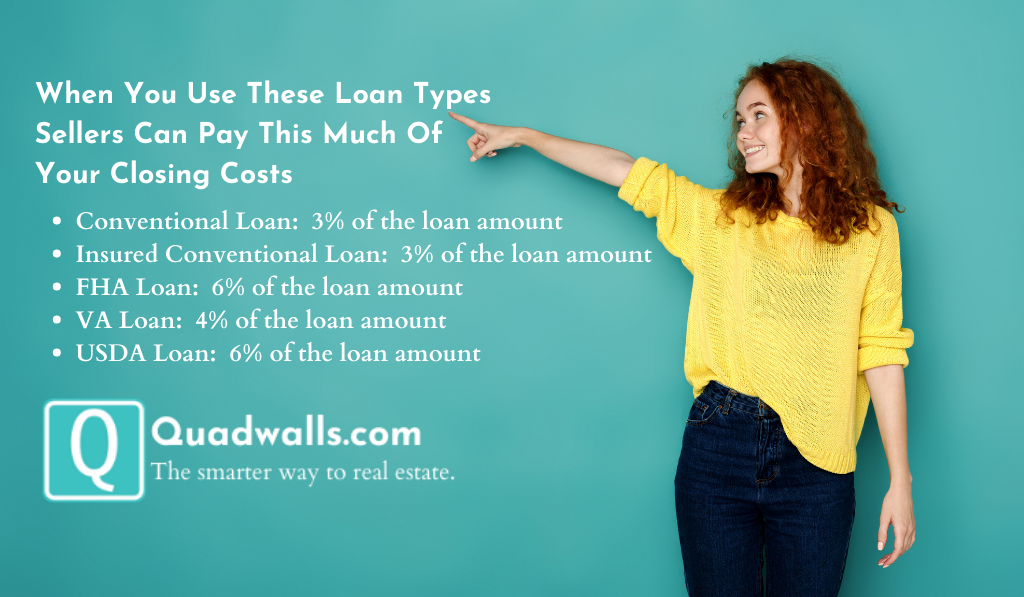

Can the Seller Pay Closing Costs?

Yes, a seller can absolutely offer a closing cost credit or a concession to offset the closing costs. This is the most common way to lower how much you need to buy a house. A closing cost credit directly decreases how much money you need to buy a home.

Home loan types limit how much as a percentage of the loan amount the seller can offer you as a credit.

- Conventional & Insured Conventional Loans: 3% of the loan amount

- FHA Loan: 6% of the loan amount

- VA: 4% of the loan amount

- USDA Loan: 6% of the loan amount

Also, there is no point in asking for a larger closing cost credit than you need. The rule for all loan types is to use it or lose it when it comes to a closing cost credit. The seller cannot pay anything towards your down payment. This leads to our next section.

Can I Borrow Money to Get My Down Payment?

No, you cannot borrow money to make your down payment on a home. Additionally, the seller cannot pay any portion of your down payment with a credit. The down payment often makes up the majority of how much money you need to buy a house.

Homebuyers can get a qualifying gift from a qualifying relative. Alternatively, homebuyers can seek down payment assistance from government sponsored down payment assistance programs.

Conclusion to How Much Do You Need to Buy a House

This was a lot of information to cover in one short post. The home’s purchase price, the down payment requirements of your loan type, and how much in closing costs you can get the seller to cover all directly affect how much you need to buy a house.

A general answer to how much you should save to buy a house is this: Buyers need to have 4% to 7% of the home’s purchase price before considering buying a home. However, if you are using a 0% down program such as the USDA or VA loan types, buyers usually just need 2% to 3% of the home’s purchase to buy a house.

How Can Quadwalls.com Help You

Quadwalls.com is the smarter way to real estate. Quadwalls.com is dedicated to helping home buyers and sellers save money and make better decisions when buying or selling homes. We can help you find and buy your new home.

Use the Quadwalls.com Home Finder Assistant to tell us what you are looking for in your new home. We will use your answers to identify the very best matching homes for your criteria and then send those to you.